Lions Bay Q4 2021 Commentary

For the fourth quarter of 2021, the Lions Bay Fund was up 10.00% and finished 2021 up 46.02%, net of all costs. Despite the strong returns for the market, it was a highly volatile year, which allowed us to benefit from gains across all three of our strategies. Senior Portfolio Manager, Justin Anis, explains how his returns this year were about much more than opportunistic hedging and active trading.

MANAGING GROWTH

For the fourth quarter of 2021, the Lions Bay Fund was up 10.00% and finished 2021 up 46.03%, net of all costs. The S&P 500 was up 11.01% for Q4 and up 28.67% for the full year. Since inception, the Lions Bay Fund has generated an annualized return of 17.80%, net of all costs, with a correlation to the S&P 500 of 0.55.

The Lions Bay Fund enters the new year with assets under management (AUM) of just over $77.5 million, up from $36.7 million at the start of 2021. When we drafted our Offering Memorandum, we included the flexibility to close our fund to new investors for at least six months once our AUM reached $100 million. It remains our intention to do so. We will always do what is in the best interests of our clients and will never prioritize asset growth over our ability to generate strong risk adjusted returns.

YEAR IN REVIEW

2021 was an exceptional year for the Lions Bay Fund. Despite the strong returns for the market, it was a highly volatile year, which allowed us to benefit from gains across all three of our strategies. Our largest holdings in our core portfolio outperformed the market, while the volatile environment allowed us to realize significant gains from active trading and opportunistic hedging.

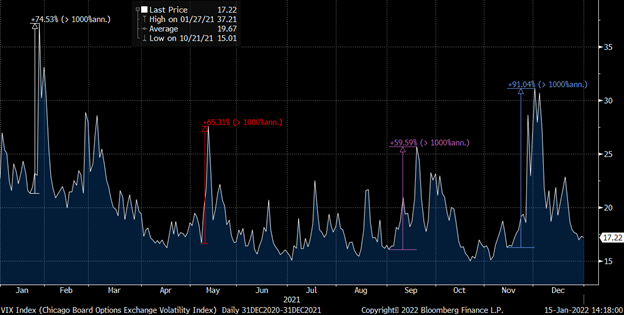

Historically, 20%+ years for the market are accompanied by subdued levels of volatility (as measured by the VIX, or volatility index). For example, in 2017 the S&P was up 21.8% with an average VIX of 11.09 while in 2019, the S&P was up 31.5% with an average VIX of 15.43. Despite the almost 30% return for the S&P 500 this year, the VIX averaged 19.67, and in four separate instances the VIX spiked over 59%. Our Fund is designed to protect and profit from bouts of volatility, as each of these instances allowed us to realize profits on our hedging tools and capitalize on short term trading opportunities.

VIX INDEX DURING 21

THE RETURN OF ACTIVE MANAGEMENT

Unlike in 2020 when stocks seemed to move in lockstep with one another, correlation among stocks declined meaningfully this year. This created a very attractive environment for active management and stock picking. The year was characterized by several violent rotations between sectors that one could miss simply looking at the performance of the S&P 500. Success in this market depended as much upon what you owned as what you were able to avoid.

The S&P 500 only had a maximum drawdown this year of 5.21%, occurring over a 21-day period in early September. It took only 13 days to regain new highs by mid-October. In contrast, the Nasdaq had a 10.5% correction in January 2021, along with a 7.8% pullback in the spring, 7.3% in the fall and 6.7% at the start of winter, while the Russell 2000 Index of smaller companies suffered a 12% drawdown at one point this year..

Our investors will know that we have been underweight technology for much of the year and were particularly cautious on the high growth/speculative stocks. We felt that the crowded nature of these trades, in combination with extreme valuations and the sensitivity of these stocks to rising interest rates, made them excellent hedging candidates for us to manage the risks of rising inflation and a potential unwind of the exuberant speculation we were observing. These hedges performed exceptionally well in the latter half of the quarter and continue to do so in early 2022, significantly outweighing the declines in our core portfolio.

MONETARY POLICY: RACING TO A RED LIGHT

As our readers will recall from our Q3 commentary, entering the fourth quarter we felt the Fed was behind the curve in combatting inflation. We wrote that everything in this cycle was happening quicker, including the speed of the sell off and the rapid recovery of the labour market:

“Investors must expect monetary policy to tighten faster than in past cycles. Yet investors remain complacent that the Fed is their friend. It is going to be a harsh wakeup call to some when they realize that the adage ‘don’t fight the fed’ works both ways.”

-Lions Bay Fund Q3 2021 Commentary

The wakeup call arrived on the morning of Wednesday November 10th during President Biden’s speech at the Port of Baltimore:

“The irony is people have more money now because of the first major piece of legislation I passed. You all got checks for $1,400. You got checks for a whole range of things. It changes people’s lives. But what happens if there’s nothing to buy and you got more money to compete for getting [goods]? It creates a real problem,”

-President Joe Biden, Port of Baltimore, November 10th

The President told the world that continued fiscal largess was creating more problems than it was solving. At the time, the market was still uncertain as to how seriously the administration was taking the inflation issue, particularly since Biden had yet to nominate Fed Chair Jerome Powell for reappointment. Some pundits expected Biden to nominate a more dovish candidate, perhaps one who embraced the easy money polices of Modern Monetary Theory. In his speech, the President indicated that inflation was a major political issue for him, which we took as a strong sign that Powell would be reappointed.

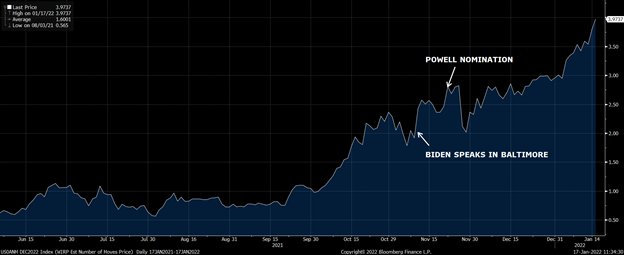

The chart below shows the number of 2022 interest rate hikes the market is pricing in over time, and we’ve annotated it to show where the narrative shifted. Recall that as late as June 16th, Powell coined the head-scratching phrase “we’re talking about talking about tapering”, at which time markets were pricing in ~0.5 rate hikes in 2022. Fast forward just 6 months and the market is now pricing 3.9 rate hikes in 2022. The Fed has moved far beyond “talking about talking”: they announced tapering of their QE program, then subsequently accelerated the timeline to finish tapering by March and are now signaling implementing “quantitative tightening” at some point this year. There is even growing speculation that they could hike rates by 50 basis points (rather than the typical 25 basis points) at their March meeting, something that hasn’t occurred in almost 22 years.

NUMBER OF 2022 RATE HIKES EXPECTED

We try and keep things very simple when it comes to understanding monetary policy. As outlined in our previous commentary, shrinking liquidity is bad for equities, in particular high growth and high multiple equities. Historically, it leads to increases in volatility. We were bearish in our Q3 commentary due to shrinking liquidity, and now that it is occurring faster than we had anticipated, we have been incrementally more bearish towards equities in general and specifically to high multiple stocks.

Powell was nominated on November 22nd, 11 days after the Baltimore speech. That morning, the Nasdaq hit a record intra-day high of 16,200 before reversing and closing red on the day (an “outside reversal” for the technical analysis fans that are reading). At the time of writing, it has pulled back over 10% from those levels in a highly volatile fashion. In December alone, the Nasdaq experienced >1% swings on more than half the trading days, including a stretch where it did so in 7 of 8 days straight. As we wrote in our last quarterly comments, periods of tightening liquidity are historically characterized by periods of elevated volatility, and this episode is proving no different. Lions Bay was well positioned for this increase in volatility, and we were able to reap significant trading gains in December. We have continued to generate significant gains from our bearish positioning in the early days of 2022, as the rapid decline in the S&P 500 and Nasdaq has pushed most of our hedges deep in the money, driving our portfolio into a net short position for much of December and the first half of January.

One standout trade for us was a bearish bet on the recently public Electric Vehicle companies. In Q4 we generated significant profits from a large put trade in this sector. Rivian Automotive and Lucid Motors were still trading close to all-time highs in mid-November, the time when we observed a significant shift in the inflation narrative. Shares were trading at ludicrous valuations, despite a significant increase in competition from traditional vehicle manufacturers. A successful short requires a catalyst, and we felt that the tightening liquidity conditions, and higher rates could spark a substantial re-rating in these shares. We felt this was an exceptional opportunity to hedge our portfolio against a growth scare and bought puts expiring in December.

On November 16th, Rivian Automotive (RIVN) was trading at a market cap of over $150 billion and a 42x sales multiple and Lucid Motors (LCID) was trading at a market cap of over $90 billion with a 40x sales multiple. On the same date, Ford and GM were trading at a market caps of $79 billion and $150 billion and 0.54x and 0.6x sale multiples, respectively. The valuations of RIVN and LCID even made Tesla look cheap – and that is saying something – with Tesla trading at a humble 13x sales multiple. Both RIVN and LCID would decline over 30% in the following weeks, and we realized meaningful gains for our active trading portfolio helping to protect our core portfolio from the broader market decline.

BACK TO BASICS

Of course, our returns this year were about much more than opportunistic hedging and active trading. The largest component of Lions Bay is a low turnover, core portfolio of long-term investments in outstanding businesses. In 2021, our largest and longest held investments delivered market beating returns. Active trading and hedging positions us to be able to add to these exceptional businesses during periods of volatility.

Houlihan Lokey (HLI), our largest and longest held holding in the fund, was up over 57% in 2021 and was the largest contributor to profits this year. As of the quarter ended September 30th, TTM revenues increased 74% from $1.12 billion in Q3 2020 to $1.95 billion in Q3 2021 and earnings per share over the same period increased 104% from $2.97 to $6.25.

In Q4, we had the opportunity to meet David Preiser, Co-President of Houlihan Lokey. A 31-year veteran of HLI and an expert in transactions involving financially distressed companies, Mr. Preiser helped found their restructuring practice and has been instrumental in leading their expansion into Europe and Asia. We came away from this meeting with even greater conviction in the long runway of growth ahead for this franchise, and the resiliency of their cyclically balanced business model. This is a business that we hope to own forever.

Airboss of America was our second largest contributor to returns this year, with shares up 196.1% in 2021. The Airboss management team has continued to execute at a high level and create value for shareholders following their blockbuster year in 2020. Continued meaningful contract wins in their healthcare and defense businesses allowed the franchise to maintain momentum while their more cyclical end markets continued to recover. The company recently raised their pipeline of potential contract wins to $1.5 billion from the $1 billion previously disclosed on their Q3 conference call.

Other top contributors for our core portfolio this year were Brookfield Asset Management (+47.8%), Live Nation Entertainment (+62.8%) and Liberty Media Formula One (+48.4%). Our worst performing trades for the year were our oil tanker stocks. These are deep value shares that continue to be hurt by the halting recovery in mobility as continuing Covid waves and travel restrictions delay the recovery in oil and jet fuel demand. We continue to believe in the recovery of the end market for these businesses, but we are closely watching credit spreads as we enter a tightening cycle – these are highly indebted companies, and our thesis would change quickly if we saw a significant deterioration in corporate credit markets. Las Vegas Sands was also a drag on performance in 2021, again due to a delayed recovery in travel due to Covid, but also over risks relating to Chinese government policy in Macau. These risks appear to have abated with the latest legislation dropping government approval of dividends, and shares are off to a strong start in 2022, up over 18% in the past three weeks.

THE PATH AHEAD

Looking at the year ahead, we remain defensively positioned and have yet to meaningfully increase our net exposure beyond rolling our hedges down in strike and out in time. While markets have had a rocky start to the year, we do not believe we are at the point of maximum pessimism or capitulation in equities, although it certainly feels like we are oversold in the short term. We continue to believe that we are in a healthy correction, which will see the unwinding of the exuberant speculation that has characterized the post-Covid rally in financial markets. This is a welcome development for long term investors and this environment will reward active managers who are prudently positioned and have the tools to profit and protect from rising volatility and falling stock prices.