Bonfire of the Volatility

Senior Portfolio Manager Justin Anis explains how the Lions Bay risk management philosophy helped deliver the Fund’s best month ever for performance relative to the S&P 500 in September. Up +32.75% year-to-date, Lions Bay is positioned defensively into year end for several reasons outlined here.

For the third quarter of 2021, the Lions Bay Fund was up +6.07%, bringing year-to-date returns to +32.75% net of all costs. These returns compare favourably to the S&P 500, which was +0.58% for the quarter and +15.91% YTD. The Lions Bay Fund marked an important milestone in Q3, as we celebrated our three-year anniversary at the end of August. Since inception, the Lions Bay Fund has generated an annualized return net of all costs of +15.79%, a total return of +59.01% and ended the quarter with $61.4 million in assets under management.

Most of our profits for the third quarter came during the month of September, when the S&P 500 dropped -4.65% in its largest drawdown since March 2020. At the conclusion of our Q2 commentary, after laying out several risks concerning us, we stated that we would be steadily reducing our exposure to equities and that we anticipated our risk management tools and hedges would be significant profit centers during the back half of the year. This was indeed the case, and our caution paid off handsomely in September as the Fund generated a return of +6.33%, marking the best month for outperformance, or ‘alpha’, in the life of the Fund. Later in this commentary, we will discuss our hedging philosophy further and our process that drove these gains.

In addition to our hedging profits, our core investments delivered strong gains during the quarter as many of our largest and longest held investments such as Brookfield Asset Management, JPMorgan Chase, US Bancorp and Houlihan Lokey all outperformed the market. Houlihan was once again our best performing investment in the quarter, and shares are up over 51% year-to-date at the time of writing. Our transactional portfolio also delivered profits as our trades tied to energy inflation had a strong month in September, led by a small position in Methanex which was up 42% for the quarter, and long dated call options in Cameco. We have exited both positions.

We believe that we are in the early stages of a correction and remain defensively-positioned with low exposure to equity markets. While we are cautious on the market, and are positioned for continued equity weakness, we want to be clear that we expect this to be a typical mid-cycle correction, not the end of the bull market.

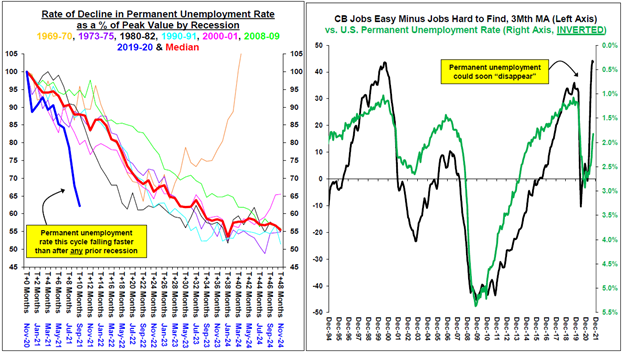

It seems odd to consider the economy at mid-cycle when we are less than 18 months removed from the depths of the pandemic, yet everything about this cycle is happening quicker. The shutdown in economic activity was instantaneous. We experienced the most rapid sell off in stocks in history, with the market down 33% in 22 days. The monetary and fiscal responses from governments were immediate, decisive, and massive in magnitude, and we experienced the most rapid doubling of stock prices in history, as the S&P 500 rallied 100% in 354 trading days. It should come as no surprise then, that the labour market has rebounded faster than in any past recession. We are now at a level of mid-cycle employment that necessitates removing liquidity from the system. The charts below make this case.

The chart on the left shows the rate of decline in the permanent unemployment rate as a percent of the peak value in every past recession since 1969. Each coloured line represents a different recession, with the bold red line representing the average, and the blue line representing the latest recession. At ten months removed from the peak levels of permanent unemployment, this level is already down to 60% of the peak. Observing the average of past recessions, it took 28 months for levels to decline to 60% of their peak levels. Ten months after the peak levels in the 2008-09 recession, we had only declined to 80% of peak unemployment. Logically then, investors must expect monetary policy to tighten faster than in past cycles. Yet investors remain complacent that the Fed is their friend. It is going to be a harsh wake up call to some when they realize that the adage ‘don’t fight the fed’ works both ways.

We remain concerned about many of the market risks we laid out in our previous commentary: exuberant sentiment, overvaluation and looming fiscal and monetary policy shifts. While some of the euphoric sentiment has come out of the market in recent weeks, this quarter has introduced new risks that we did not previously foresee.

Crackdowns in China that were initially targeted at high-flying technology companies and data security have evolved into a broad crackdown in pursuit of “common prosperity”. This comes during a time of significant credit stress amongst Chinese property developers and increases the risk of a policy error by the Chinese government if they fail to contain the fallout of the Evergrande restructuring. We’re certain Evergrande will be getting best in class counsel during this process – they retained Houlihan Lokey as their restructuring adviser.

The chart below shows the China Credit Impulse 12 Month Net Change, which is calculated by Bloomberg Economics. Essentially itmeasures the change in the levels of liquidity in the Chinese economy. As you can see, liquidity has tightened up considerably inrecent months. This measure has proven to be a leading indicator for global manufacturing activity.

Supply chain issues continue to challenge the economy, and investors are realizing that these pressures are not as ‘transitory’ as they had initially hoped. One must believe this is the case when the very people who have championed the word transitory and included it in every discussion of inflation since the financial crisis – the Federal Reserve – are finally coming around on it.

“It is becoming increasingly clear that the feature of this episode that has animated price pressures — mainly the intense and widespread supply-chain disruptions — will not be brief. By this definition, then, the forces are not transitory”

-Federal Reserve Bank of Atlanta President Raphael Bostic in prepared remarks to the Peterson Institute of International Economics, October 12th 2021; Bostic is a voting member on policy this year.

We believe the quarterly earnings season that is about to begin will provide much more clarity on how serious these issues are and presents a risk that many companies will miss earnings and cut full year guidance. We do not believe equities have appropriately priced in this risk as the price action of recent bellwethers such as Nike and FedEx demonstrated following their recent earnings stumbles blamed on supply chain issues (FDX -11% after earnings September 21st, NKE -6.2% after earnings on September 23rd). Input cost inflation and rising procurement costs will ultimately have to be passed on to consumers, who are already facing rapidly rising food, energy and lodging costs.

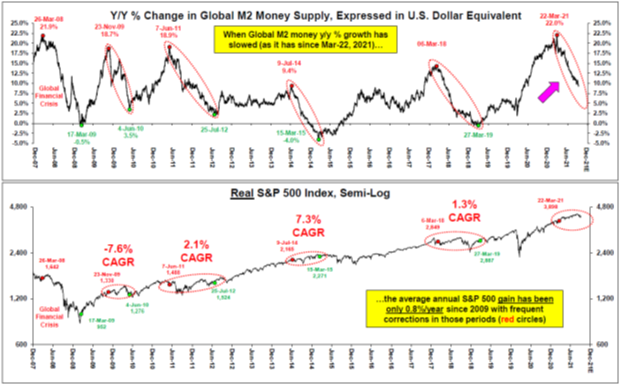

Stanley Druckenmiller, renowned hedge fund manager and an investor we hold in very high regard, has stated “most people are looking for earnings and conventional measures. It’s liquidity that moves markets.” By liquidity, he is referring to the global money supply which is driven by central bank policies. Markets love liquidity, and decisive actions by central banks to flood financial markets with liquidity helped prevent a health crisis from turning into a financial crisis. In a win for humanity, the roll out of effective vaccines has likely put the worst of the health crisis behind us. In a challenge for financial markets, this means scaling back much of that emergency liquidity.

The chart below highlights the year-over-year change in global money supply in the top chart, with the performance of the S&P 500 shown below. The time periods circled in red signify periods where liquidity/money supply is decreasing. The S&P 500 performance during these periods has been characterized by high volatility and poor returns. The average annualized return during such periods is 0.8% since the financial crisis – a stark difference from the long-term average returns for equities. As the Federal Reserve begins to taper its bond purchases this quarter, with a target of ending QE entirely by the middle of 2022, this measure will tighten further, and we expect the historical relationship of rising equity volatility to play out. As our clients know, we relish volatility, and we have the tools to protect and profit during such periods.

This quarter provided a great case study to examine the hedging philosophy and strategy at Lions Bay. We take both a systematic and an opportunistic approach to portfolio hedging. Regardless of our market view, we will almost always have some protection in the portfolio in the form of put options on equity indexes such as the S&P 500 and the Nasdaq1. This is the systematic portion of our risk management, and its function is to protect our investors from unforeseen market risks and black-swan type tail-risk events. As a compliment to this strategy, we also use hedging tools opportunistically when we feel that there is a disconnect between how the market is pricing risks on a certain sector or stock, and our view of the risk. When we perceive a large disconnect between the pricing of risk in the market and our perception of risks, we will be more aggressive with our hedging practice.

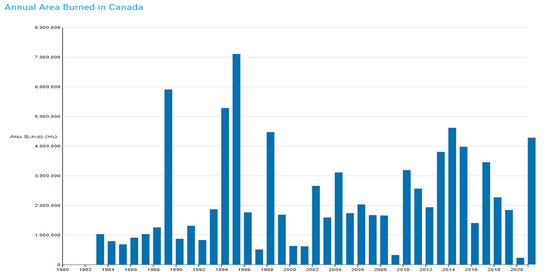

We believe that the phenomenon of forest fires is analogous to the way we think about risk management. This summer, Western Canada suffered terribly from wildfires in a dire reminder of the threats posed by climate change. Total hectares burned in Canada were the highest since 2014 and the second highest since 1998. What is interesting to note however, is that 2020 saw the lowest hectares burned in over 20 years. As long periods pass without fires, excess dry brush and dead vegetation build up, leading to more catastrophic fires in the future.

The same dynamic plays out in volatility markets. As markets continue to march higher in an orderly fashion, investors get more comfortable with risk, financial leverage increases and complacency sets in, setting the stage for more catastrophic sell offs in the future. As this happens, the price of volatility declines, meaning it is increasingly cheaper to hedge a portfolio against declines while the potential hedging gains and have only increased in magnitude and probability. Put simply, investors think that because there hasn’t been a fire recently, the likelihood of a fire in the future has decreased. The reality of course is just the opposite, and it is this inefficiency that we seek to capture by opportunistic hedging.

Equity markets experienced an uneventful summer, and volatility continued to trend downward into Labour Day as the S&P 500 notched its 7th straight monthly gain. The S&P was enjoying its 4th longest stretch without a 5% pullback in 50 years, while the VIX, which measures equity volatility, notched its sixth lowest weekly close of the year on September 3rd. Meanwhile, we were fretting over many of the risks we’ve discussed above.

When we see a set up like this, a total disconnect between the pricing of risks and our perceptions of them, we will go beyond our normal course systematic hedging and be opportunistic and aggressive. In addition to increasing our level of index hedges, we bought puts on a select group of large cap equities, and in a direct bet on volatility, we bought call options on the VIX index. These actions paid off well for us in September, as the S&P 500 finally managed to snap its win streak, declining 5.6% from the Sep 2nd highs of the month to the lows at month end. It did so in violent fashion, with the VIX rallying 83% in 11 trading sessions in a win for our call options.

We hope this case study helps our investors understand how we think about risk and demonstrates the value of active portfolio management. Our core investment portfolio will deliver the majority of our returns over a full market cycle, but we have the tools to profit and protect during periods of equity weakness as well.

1We say ‘almost always’ because there are times in the depths of a panic that continuing to buy volatility does not make any rational sense – we don’t wish to join the stampede of investors looking to buy insurance once their house is already on fire. When these rare periods occur, we view them as opportunities to buy, not sell stocks