Lions Bay Q2 2020 Commentary

Lions Bay Fund portfolio manager Justin Anis discusses Q2 gains and the resurgence of the day trader.

For the second quarter of 2020, the Lions Bay Fund was up +9.51%. Year-to-date, the fund is down -0.09% while the S&P 500 is down -3.08% over the same period. Returns for the second quarter were driven primarily by our core investment portfolio, although it was also a very profitable quarter for short-term trading. Our portfolio hedges were a drag on performance during the quarter as volatility declined.

In our core portfolio, our best performing investment in Q2 was Airboss of America, whose shares rose 126% during the quarter. Airboss trades on the TSX (BOS-T) and is an industrial company specializing in custom rubber compounding. They serve a diverse group of end markets including automotive, heavy industry, construction and defense. We have owned shares in Airboss since the inception of Lions Bay. We were attracted to the strong management team and compelling valuation, as well as their growing defense business. Chairman and CEO Gren Schoch is an entrepreneur with an enviable track record of growing businesses, particularly in cyclical industries, and owns over 20% of the company personally. We have met with him several times over the years as part of our research process and he has always spoken to the growth potential of their defense group. His management team’s focus on the defense business bore fruit in late March, as their subsidiary, Airboss Defense Group, was awarded USD$96.4 million from FEMA to produce Powered Air Purifying Respirators for medical personnel and first responders in the battle against COVID-19. Such a meaningful order is a testament to the quality of solutions and technology that Airboss can offer and of their ability to respond rapidly to the emerging needs of government agencies.

Source: Bloomberg

Our next three best performing stocks were Amazon, Apple and Microsoft. The pandemic drove demand for Amazon’s services and allowed the company to win over the last of the e-commerce hold outs. Remote work only further drives the already insatiable demand for cloud computing power, which Amazon Web Services provides. Microsoft benefitted from similar trends through widespread adoption of their cloud computing solutions, meeting over Microsoft Teams, as well as an increase in demand for their gaming franchise as video games were a massive beneficiary

from lockdown measures. Apple benefitted from further adoption of their Services business, which should continue to grow and improve the corporate margin profile.

The success and growth of these franchises is no secret and we believe is well priced into their shares. As such, we have trimmed our exposure to each of these companies into the massive rallies they’ve enjoyed year-to-date, selling our positions by around 60-70%. The amount of crowding in large cap technology stocks makes us uncomfortable, and we know that a great business is not always a great stock. The dominance of all the aforementioned franchises is difficult to overstate, yet we believe their current share prices represent full value and present little room for error.

While the header to this commentary shows all three companies in the top ten holdings, at the time of writing, none of them remain there.

The chart below shows how extreme the divergence has been between growth and value stocks, and believe a potential rotation represents a risk to these companies and an opportunity for Lions Bay investors. We have begun to selectively buy shares in oversold and out of favour companies – known as “value stocks” to position our investors to profit from this divergence. Specifically, we have targeted short-cycle industrial stocks with exposure to housing, automotive, forestry and construction – all of which enjoy the tailwind of an extended period of low interest rates.

Source: Bloomberg

Houlihan Lokey rounds out our top five best performing stocks during the quarter and like the large cap tech holdings and Airboss, they also saw their competitive position improve over the course of the pandemic. Shares rallied strongly throughout May on improving prospects for their restructuring franchise, and the stock was up over 30% on the quarter by mid-May. We were sellers into this strength, cutting our position from 7% to 3%, and it looks like management shared our opinion that the shares were approaching full value. On May 18th, with shares at an all-time high of $64.39, management raised $190 million through a stock offering priced at $63.50. We commend the management team for opportunistically raising capital at such levels and believe they will deploy it in an accretive fashion through acquisitions which should further drive shareholder. We have been buying stock back in the mid-50s. The next quarter will be challenging for Houlihan as there is a timing mismatch between when their restructuring revenues can be realized to offset an immediate drop off in their corporate finance business. We would view any pullback post earnings on July 28th as a buying opportunity and believe the restructuring opportunity ahead of Houlihan is massive. In the last week of Q2, thirteen U.S. companies sought bankruptcy protection, the most of any week since May 2009 in the depths of the global financial crisis.

Our transactional portfolio had a strong showing in the second quarter, and we were able to capitalize on many short-term trading opportunities that the COVID-19 crisis presented. The lion’s share of the gains (pun intended) for this strategy came from lumber stocks. Some investors will recall our lumber windfall from August of 2019, when our holding in Canfor

soared close to 73% in one session as a result of a $15 take-private bid for the company by insider James Pattison, who owns over 50% of the shares. We sold our entire position over the days following the announcement.

In late December 2019, minority shareholders objected to Pattison’s $15 bid, claiming that it undervalued the company. To summarize: Mr. Pattison thought it was a great buy at $15. Most of the minority of shareholders thought $15 was too low. Thus, when shares were trading below $8 in March, we were buying with both hands. Apart from the evident value in the shares, we believed that lumber would be a beneficiary from the COVID crisis as lower interest rates stimulate new home construction, while stay-at-home orders drove demand for lumber for

renovations and DIY projects at home. In addition to Canfor, we also initiated new positions in West Fraser Timber and Interfor, both of which stand to benefit from rising lumber prices.

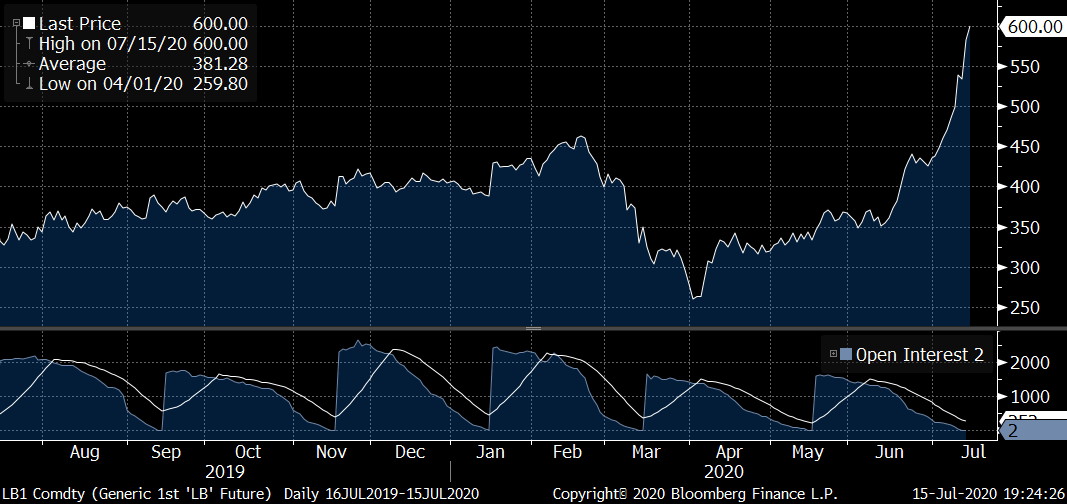

In our opinion, our thesis played out well this quarter and continues to do so early in the third quarter. A massive increase in lumber demand coincided with a drastic reduction in supply, as production was curtailed in response to lockdown measures, as well as in response to the initial drop-off in demand in March. Lumber mills do not operate like a light switch, and it can take weeks to bring curtailed output back online. A Wall Street Journal article on July 9th spoke to the phenomenon, and the chart below highlights the parabolic move in lumber prices year-to-date. “People didn’t go on vacation,” said Leiby Wieder, who manages Tri-State Lumber in Brooklyn, N.Y.’s Greenpoint neighborhood. “They stayed home and built decks, they built fences, they built pergolas. Anything and everything.”

Source: Bloomberg

We have been steadily trimming our lumber investments since the start of the third quarter, as the share prices of these companies are rapidly beginning to close the gap with their fundamentals. At the end of the second quarter, we owned Canfor, West Fraser Timber and Interfor, which collectively amounted to 4.4% of the Fund and contributed approximately 140 basis points of positive returns for the quarter. At the time of writing, we have divested completely of our holdings in Interfor and our combined weight in Canfor and West Fraser is just over 2.6%. We have a strong respect for the philosophy that when one’s trade appears on the cover of the Journal, one must take profits.

We feel that we must comment on the much discussed ‘day trader’ phenomenon that the financial media is so worked up over. The growth in retail trading, spurred by commission free trading and accessible trading platforms such as Robinhood, combined with outspoken personalities like Barstool Sports Founder Dave Portnoy, has provided some juicy material for financial pundits. Indeed, we even recently received a report from a strategist at a U.S. brokerage firm entitled “The Portnoy Top”. Despite all the gnashing of teeth and angst over the growth of retail trading, we do not view this development as a negative, let alone a sign that the end is nigh. We understand that with casinos and sports betting closed and weekly stimulus cheques in the mail, it is a compelling story to suggest that speculators have moved to the stock market to get their fix. We are not frightened nor surprised by this. We believe speculation is inherent in human nature, whether it’s tulips or tech stocks. We think it is terrific that a younger generation is getting exposure to the investment world and are excited by the prospect of a new cohort of investors entering the picture. From the perspective of a portfolio manager of a long short hedge fund, we are thrilled by these developments. Increasing retail participation in the stock market can only mean increased volatility, which means increased opportunities for Lions Bay investors.