Silver Linings - Aon

Aon’s current takeover of its rival secures the company to emerge from the pandemic stronger than ever.We explain below in the latest Silver Linings.

It has almost been one year since the initial global lockdowns and travel restrictions caused by COVID-19 began, which dramatically impacted how all businesses operate. Our goal with the Silver Linings series is to highlight unloved companies who can emerge stronger from the disruption caused by COVID-19. Greg Case, the CEO of our holding in Aon plc, highlighted this exact point on his Q4 2020 conference call, where he said “There are very few firms who can say they ended 2020 stronger than they began, and I want to thank our colleagues for making Aon one of those firms”.

Aon is a leading global commercial insurance broker. It has an impressive long-term growth track record, innovative new products, and defensive business model, as commercial insurance is largely non-discretionary. The company has exited 2020 stronger, because earlier in the year Aon announced the acquisition of one of its largest competitors Willis Towers Watson PLC. The combined company would be the largest commercial insurance broker in the world. We believe this acquisition gives Aon unrivalled scale globally to invest in innovation and data analytics. It also gives Aon a complementary set of capabilities to serve unmet needs of global customers which can help accelerate the growth of the combined company. The pandemic has increased the need for innovation and the importance of an enterprise-wide approach to risk management. According to an Aon global risk survey, six of the top ten global risks are uninsured or underinsured currently. Aon is a key partner in managing these risks and creating new products to address difficult to model risks including cyber security, climate change, and intellectual property.

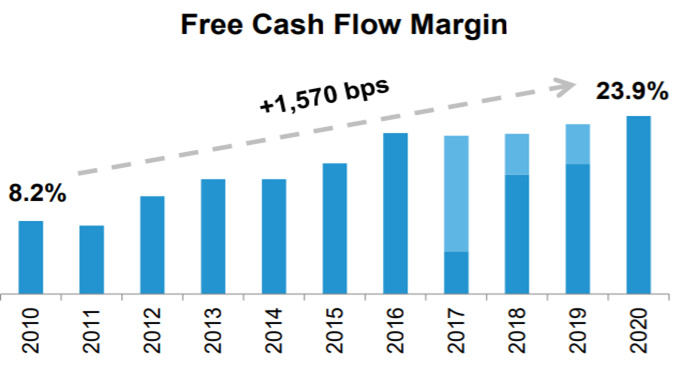

There are also considerable cost saving opportunities from the Willis Towers Watson acquisition. When Aon closed the deal, they assumed they could achieve $800 million of cost synergies, or 5% of the combined cost base. However, this is well below its past two acquisitions, which resulted in 2-3X more cost savings. Aon has commented that there is nothing structurally different about this acquisition that would prevent similar levels of cost reductions over time. This will help Aon continue to expand its operating and free cash flow margins, which it has done consistently over the last decade.

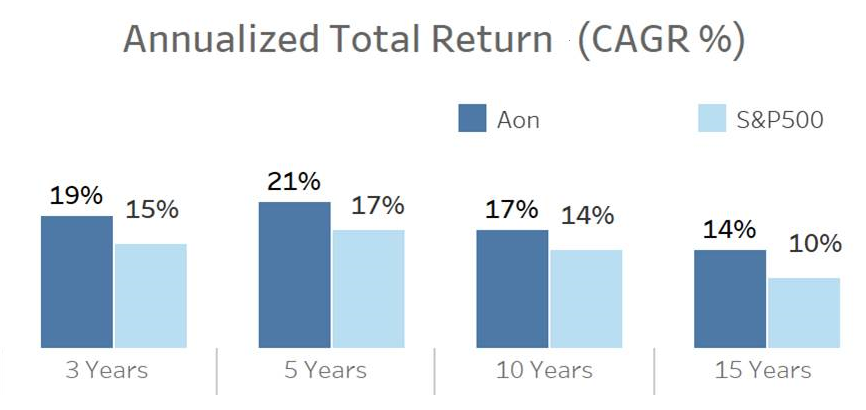

Another key attraction of Aon’s business model is the consistency of its earnings growth. This was on display in 2020. Despite the disruption caused by COVID-19, Aon was able continue its streak of growing its earnings per share every year for the past 15 years — even through the 2008-2009 financial crises. This has all been under the leadership of Aon’s CEO, Greg Case, who has been CEO since 2005 and has helped the company to outperform the S&P 500 over the past 15 years.

Insiders of the company appear to agree with our view that shares are attractively valued. In the past year, insiders including the chairman of the board Lester Knight, purchased over $15 million in equity. Additionally, in its most recent quarter, the company bought back $800 million in stock, returning a total of $2.2 billion to shareholders in 2020 through buybacks and dividends for a 4.5% yield. This is an impressive feat as many companies had to suspend dividends and buybacks in 2020 given the uncertainty. Aon has consistently bought back large amounts of stock believing its shares are undervalued. In total, the company has bought back 50% of its float since 2012. Going forward, we expect Aon to have strong growth through innovation, expanding margins, and significant free cash flow to return to shareholders, setting it up to emerge stronger from 2020.