Lions Bay Q1 2022 Commentary

Lions Bay Fund entered the year positioned extremely defensively and was able to profit from the volatile market. Senior Portfolio Manager, Justin Anis, discusses why active trading and hedging proved to be a profitable strategy this quarter.

For the first quarter of 2022, the Lions Bay Fund was up 17.1%. The S&P 500 was -4.6% over the same period. The Lions Bay Fund has now generated a cumulative return of 104.9%, or 22.2% on an annualized basis net of all costs since our inception in August of 2018.

Macro Movers

It was an incredibly challenging quarter for the markets. The tragedy in Europe escalated far beyond what many expected, as Russian saber rattling escalated into a full-blown war in Ukraine. The US Consumer Price Index (CPI) printed at 7.9% year-over-year at the end of February, the highest inflation reading since the early 1980s. The Federal Reserve hiked interest rates by 25 basis points (0.25%) and indicated they intend to hike aggressively until at least mid-2023, including the possibility of multiple 50 basis point hikes in the coming months. Furthermore, they ended their bond purchase program (Quantitative Easing) last month and indicated that at the next meeting in early May they will begin actively reducing their balance sheet (Quantitative Tightening). Their forecast for the path of rate hikes, the timing of QT and the pace at which it will occur all came in more aggressively than Wall Street was forecasting at the start of the year. All of this was hitting a richly valued S&P 500 that entered the year at all-time highs. Financial assets did not fare well in the face of all these cross currents.

Nowhere to Hide

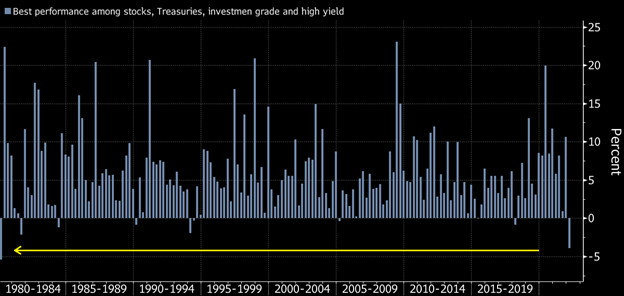

In Q1, US Treasuries fell 5.6%, investment grade bonds dropped by 7.9%, high yield bonds lost 4.8% and the S&P 500 declined 4.6%, as more than $3 trillion of value was erased from bond and equity markets. While the individual losses of each of these asset classes is meaningful on its own, what is truly significant is that all four posted such large declines at the same time. Bonds, and particularly treasuries, historically act as a buffer against declining equity markets. This is the principal behind the well-known “60/40 portfolio”. The chart below shows how rare it is for these asset classes to post such losses in concert. This was the worst quarter by this measure since 1980.

Best Performance Among Stocks, Treasuries, IG & High Yield Bonds

Despite the ominous heading in the chart above, there were in fact a couple of places to hide this quarter: commodities, and volatility. While we only had a small amount of commodity exposure in Q1, we were very long volatility, and this allowed us to profit from the market chaos.

Profiting From Volatility

As our investors will recall from our Q4 commentary, we entered 2022 very defensively positioned. As markets enjoyed a year end melt-up, or “Santa Claus Rally” in late December, the S&P 500 rallied 5% in four days to all-time highs over the Christmas holidays. The VIX, which measures the cost of hedging the S&P 500, declined by 24% over the final eight trading days of the year. In the face of this Christmas cheer, we adopted a decidedly Grinch-like approach and loaded up on cheap hedges that would protect our portfolio over the early months of 2022.

In the first three and a half weeks of January, the S&P 500 declined by 9.7%, and the VIX skyrocketed over 85%, leading to a windfall for our hedging portfolio. At the worst levels of the quarter, the S&P 500 was down over 13% from its highs, and the Nasdaq declined over 20% from the highs. As markets rallied sharply in early February, we re-loaded many of these hedges, which helped protect our portfolio when markets made new lows in March following the outbreak of war. On the February rally, we shifted the focus of our hedging activity from high-growth speculative technology stocks towards more cyclical sectors, particularly financial stocks. We will discuss this further later in the commentary.

Troubling Market Internals

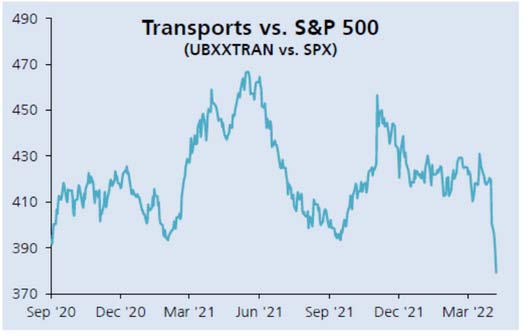

Equity markets ended the first quarter well off their worst levels, but we see several reasons for caution based on market internals. Cyclical areas of the market (i.e., those most levered to economic activity) have been trading terribly, while defensive sectors such as staples and utilities are outperforming. This type of price action is not encouraging for bulls. In the two weeks ended April 7th, the best performing sectors were Utilities +7%, Defensives +6% and Real Estate +5%. The worst performing sectors were Semiconductors -9%, Transports -9% and Banks -9%. Transports are a leading indicator of economic activity and when they underperform relative to the S&P 500 it is a red flag for the market. The chart below shows how dramatic this move has been in recent weeks.

UBS Transportation Index vs. S&P 500

We remain cautious on equity markets in the short term and respect the message the market is sending. We anticipate it will be a very choppy summer. Having said that, we are not nearly as negative on markets as we were at the end of Q4, particularly when we look 6-9 months out. Sentiment has deteriorated significantly, and equity market valuations have come down. At the end of December, markets were at all-time highs, valuations were rich, and sentiment was somewhere between greed and complacency, thus we were negative. As we write now at the end of Q1, valuations have rationalized somewhat, sentiment has soured considerably, and most market participants are calling for an imminent recession, thus we are less nervous about markets than we were three months ago: a great deal of fear has been priced into equities in the past three months.

S&P 500 Fwd P/E Ratio

Global Growth Optimism at All-Time Lows

Don’t Take the Fed at Their Word

We believe it is important for investors to appreciate that the Fed has not overtightened – yet. Actual concrete actions they have taken thus far are a 25-basis point hike and ending Quantitative Easing. Future hikes, and the pace and magnitude of Quantitative Tightening, have only been telegraphed at this point. They have plenty of runway to walk back their hawkishness should the economy deteriorate significantly, or should inflation fade as supply chain woes ease, inventories are drawn down, and tighter financial conditions are passed through to the economy. This is not the case of a central bank that has over-tightened policy and now must contemplate reversing course and taking back rate hikes. They have plenty of room to change their mind, and we believe they will be forced to.

It is our view that investors are making an error if they are basing investment decisions on the assumption that the Fed will be able to tighten according to the path they’ve laid out in the past three months. The market is currently pricing in another 8.8 hikes by year end, in addition to the balance sheet run off at a maximum of $95 billion in securities a month. We would take the under on one, if not both measures. The economy will slow down or something in the financial markets will crack before then, and they will likely have to pause their tightening. We believe this has the potential to set the market up for a year-end rally, although of course the million-dollar question is: what level will we be rallying from? Fund managers who can protect capital through the volatile first half of the year will be very well-positioned to capture such a move.

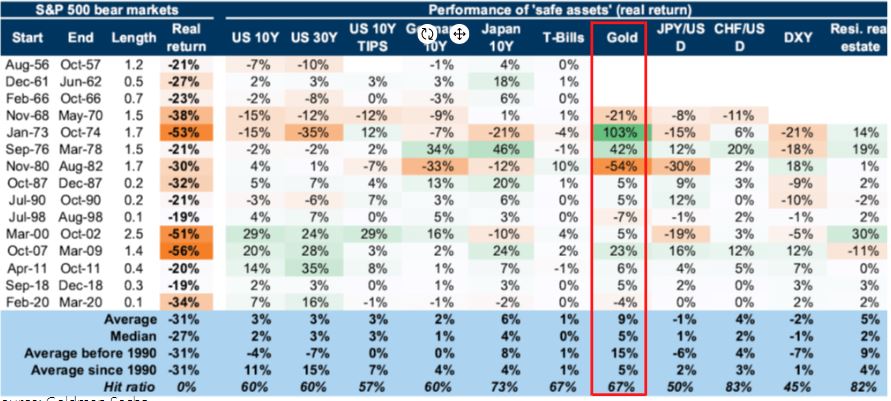

The narrative described above would also be positive for gold, and we could easily see all-time highs in gold by year end. In fact, gold should perform well for the balance of the year under several scenarios we can imagine. If the war in Europe escalates and draws in other NATO countries, gold would catch a bid on a flight to safety trade. If the economy completely unravels and drives the S&P 500 into a bear market, gold will likely outperform based on historical analogues. Looking at the past fifteen bear markets for the S&P 500, gold has generated an average return of 9% through the duration of the bear market, 50% better than the next best performing asset, Japanese 10-year bonds.

Performance of Safe Haven Assets in Bear Markets

Review by Strategy

Given the significant returns the Fund generated in Q1, we would like to provide examples of specific actions we took this quarter in each of our three strategies: the core portfolio, active trading, and hedging. We hope that these examples will help our readers better understand how we think, trade, and invest. We also hope to shed some light on current opportunities that are available to us in volatile market conditions.

Core Investment Portfolio

Our core portfolio was our worst performing strategy for Q1, as our long-term investments suffered with the broader market. Our best performing core holding was Altius Minerals, which was up 38.8% for the quarter. Our investors will recall us writing about this investment in the past – it is a long-held holding for the Fund and we view it as the best way to gain exposure to commodity prices for our core portfolio. We believe the founder and CEO, Brian Dalton, to be one of the sharpest minds in the industry and we have enjoyed following his continued success. As we mentioned earlier in the commentary, commodities have performed exceptionally well this year, and Altius also enjoyed several tailwinds this quarter. In early February they benefitted from positive drill results at their Chapada copper royalty asset, which created the potential for a significant expansion in copper production at a time when copper prices are flirting with all-time highs (and twice the level they were at when Altius acquired this royalty). They further benefitted from their potash royalties. With the disruption of potash supply from Russia and Belarus (40% of the market), potash prices are up 41% quarter over quarter and over 200% year over year. As we are less excited about commodity prices in the face of a slowing global economy, we took some profits in the stock in early March.

We were excited to add a new name to our core portfolio this quarter, LVMH Moët Hennessy Louis Vuitton, and readers can see it is now our sixth largest holding. Shares plummeted after Russia’s decision to invade Ukraine, and by early March, they were down over 28% from their January highs. We built a position in the U.S. listed American Depository Receipts (ADRs) between $121 and $128 a share. LVMH has a dominant portfolio of some of the best global luxury brands and is led by visionary CEO Bernard Arnault, who has an incredible track record of creating value for shareholders. The high margins enjoyed by ultra-luxury brands means they are well-positioned to manage through periods of inflation. It was clear to us that shares were over-reacting to the fears of Russian buyers leaving the luxury market, as LVMH’s exposure to Russia is only 2%. The ability to act decisively when we see great businesses on sale is a byproduct of our risk management process – our hedging gains enabled us to buy aggressively when most investors were in liquidation.

Investors will also note from our top 10 holdings list that we substantially increased our shareholding in Ferrari (RACE). We’ve owned Ferrari since 2019, when we had the opportunity to meet with the company in Toronto. Ferrari, like LVMH, is one of the great global luxury brands in the world. They enjoy tremendous brand power and a business model much closer to Hermes than a traditional automaker. Ferrari’s business model of maintaining production below demand leads to strong residual values and creates meaningful pricing power, which keeps them well insulated from inflation risks.

We knew from our meeting with their head of Investor Relations, Aldo Benttei, that their exposure to Russia was minimal as he highlighted their yet unreleased SUV, the Purosangue, as an opportunity to break into this market. In addition to the launch of their SUV, the company’s electric vehicle strategy is expected to result in even higher margins in the coming years. The company has guided to EBTIDA margins increasing to 40% in 2025 from 35% in 2021. For reference, the EBITDA margins for BMW are just shy of 18% and for the Mercedes Benz Group, 15%. Similar to LVMH, this was an opportunity for us to redirect trading and hedging profits to add to an incredible long-term investment that was caught up in the market panic. When we stepped in to double our position, shares were down 30% in just over eight weeks.

After being the largest contributor to our returns last year, this quarter Houlihan Lokey was our biggest detractor at -74 basis points. We were able to offset a substantial portion of these losses through hedges in related businesses, which we will discuss shortly. Houlihan Lokey declined 14.8% in Q1. This sets up a phenomenal buying opportunity for long term investors who have a good understanding of Houlihan’s business model. The shares understandably declined as M&A activity froze with the outbreak of war in Europe. Earnings estimates have come down street-wide, and we believe this is widely understood by the market at this point and largely priced into the shares. We believe the market fails to appreciate two factors.

Firstly, if credit spreads continue to widen and interest rates continue to rise, the level of Houlihan’s restructuring activity will pick up meaningfully. This allows the firm to continue to generate revenue through the cyclical downturn. Given that the revenue from restructuring engagements is longer term in nature (due to the fees structured as retainers and completion fees), and that corporate finance activity can dry up almost immediately, there will likely be a mismatch for a quarter or two as we saw in March 2020. This creates the opportunity we are in today, where most investors are unwilling to look one to two quarters out and are focused singularly on the immediate term.

The second factor is that Houlihan has demonstrated an ability to grow and gain share through economic downturns. Indeed, it is clear from our many discussions with management that they designed their firm with a counter-cyclical business model for just this reason. In 2020, they were able to attract top talent from much larger firms including the big four accounting firms, which were unable or unwilling to compensate their top talent at a level needed to retain them. With Houlihan’s counter-cyclical business model, the stability of the restructuring revenues during a downturn allows them to acquire top talent who may be disgruntled at more cyclical firms. The longer a downturn lasts, the better it will be for Houlihan Lokey. We have been buying shares aggressively in the past two weeks and would look for an opportunity to do so even further if shares over-react to a poor first quarter in early May.

Active Trading Portfolio

Active trading was a highly profitable strategy for us this quarter. Our largest profits in this book were driven by our long trades in oil tanker stocks, which rallied strongly on Russian oil sanctions. Scorpio Tankers was up 66.9% for the quarter while Ardmore Shipping was up 33.1%. We are gone from both names.

Trading in gold and gold equities was a large profit center for active trading in February and early March. By late February, volatility was trading at a level where hedging with equity options was a losing proposition. We are in the business of buying cheap hedges with an attractive risk/reward, not buying insurance once the house is already on fire. We felt that gold and gold equities, which had been consolidating for 12 months, were poised to break out on a flight to safety trade as the Ukrainian tragedy unfolded. We established a position when gold was around $1,850 an ounce, and invested approximately 10% of our assets in GDX, GLD and GDXJ. Gold rallied significantly into early March, and we realized gains of 51 basis points. We rolled most of these profits into long-dated call options, allowing us to maintain upside exposure while only risking our trading profits.

Hedging Portfolio

Lastly, a few specific trades from our hedging portfolio will highlight how we act to mitigate risk in our core portfolio. Earlier we discussed our systematic hedges, which are broad market hedges we almost always maintain (outside of when we are in the depths of a crisis and volatility is irrationally priced.) We also hedge opportunistically, based on a view we may have on a specific sector, or in this case, a specific risk we have identified within our portfolio. When markets staged a powerful rally in early February, we began to build large hedges against financial stocks. We wanted to hedge our large holding in Houlihan, which we knew would suffer if our market view played out, and we felt that the risk reward on these hedges was compelling. By February 9th, a basket of financials as measured by the XLF ETF, had rallied right back close to all-time highs (see chart below).

Financial Select Sector ETF (XLF)

Investors and traders were responding in knee-jerk fashion to the move higher in rates, as the ‘textbook’ says to buy financials when rates rise. What matters much more than the absolute level of rates is the slope of the yield curve. If rates are moving higher absolutely but the yield curve is flattening, this is not good for financials. Banks borrow short and lend long, higher long rates don’t mean much if the short end is rising commensurately. Furthermore, a flattening yield curve coupled with higher rates indicates slowing economic activity, a risk to the banks’ credit portfolios and future investment banking engagements if default risks rise.

We built a diversified basket of hedges expiring between mid-February and mid-May, and were able to realize substantial profits over the course of March, which helped offset the declines in our portfolio. March 11th puts on a large, bulge bracket US investment bank earned 18.7 basis points, March 18th puts on a European M&A advisor with a large asset management franchise delivered 8.2 basis points and puts on two U.S. based middle-market investment banks delivered a further 16.5 basis points of gains. Combined with a basket of puts on the US Financials ETF with expiries between Feb 18th and Feb 25th, which generated 24.1 basis points, these hedges generated a total of 67.5 basis points of realized gains in the quarter. This went a long way towards mitigating the decline of our largest investment and positions us well to redirect these profits to substantially increase our position in HLI at a time when it is trading cheap.