Pause on Expectations for a Fed Pivot

The award winning Lions Bay Fund finished 2022 up +39.75%, net of all costs. Senior Portfolio Manager, Justin Anis, shares his year in review and his 2023 outlook regarding inflation and rising unemployment.

Performance

For the fourth quarter of 2022, the Lions Bay Fund was up +10.57%, bringing return for the full year to +39.75% net of all costs. This compares very favourably to the S&P 500, which was up 7.54% for Q4 and finished 2022 -18.12%.

Lions Bay Business Update

The Lions Bay Fund was awarded First Place in the category of “Best 3-Year Sharpe Ratio” at the Canadian Hedge Fund Awards in November. The Sharpe ratio is a performance metric that aims to quantify risk-adjusted returns – a fund that generates strong returns without high volatility would score well on this metric.

The Fund enters 2023 with approximately $150 million in assets under management. To date, our growth has not impacted our ability to execute our investment strategy, but we remain committed to growing in a prudent and measured fashion.

Year in Review – A Bubble Bursts

Last year was an exceptional year for Lions Bay. The market conditions present in 2022 were exactly the type that Lions Bay was designed for – high levels of volatility across asset classes with meaningful dispersion between single stocks and industry sectors.

The first half of 2022 saw the unwinding of a large bubble in speculative growth stocks. Our readers know that our number one concern heading into 2022 was the risk of a disorderly rise in interest rates, as the Fed abandoned the term ‘transitory’ to describe inflationary pressures, and got serious about controlling spiraling prices.

In our commentary one year ago, we highlighted a speech that President Biden made on November 10th, 2021, when he spoke candidly that inflation was his number one priority, and was now a big political issue. Jerome Powell was nominated for a second term twelve days later, and it was clear to us that the market was underpricing a risk of sharply tighter monetary policy. We don’t think it’s a coincidence that the Nasdaq peaked at its all time high two days before this nomination.

The vast majority of our 2022 gains early in the year were earned by being on the right side of the speculative bubble popping. Similar to hedge funds who reaped outsized gains in 2007 and 2008 when the housing bubble popped, it wasn’t just about having the right call on market direction but using the right instruments. Like the Credit Default Swaps which paid off many multiples of the premium paid to implement them, our put options on some of these speculative stocks and ETFs allowed us to earn a similar payoff profile.

When hedging the broader market, we generally employ put spreads, which cap our profit potential at a market decline of somewhere around 15-25% for the S&P 500. We aren’t in the habit of betting on the world ending. As the saying goes, it’s not a great bet as it only happens once.

Companies, however, are a very different story. We felt that if some of these speculative stocks cracked, particularly those in the Electric Vehicle space, “Innovation” sector and those exposed to the cryptocurrency ecosystem, weren’t going to stop declining down only 15-25%. We felt there was a genuine possibility they would fall in line with the average decline of a Nasdaq stock post the 2001 bubble bursting – the Nasdaq declined 78% peak-to-trough from its March 2001 highs. We felt that now, like then, there was just no defensible valuation floor for many of these businesses.

Cathie Wood’s ARKK ETF, the poster child of the speculative bubble, managed to exceed the Nasdaq bubble pullback, having suffered a peak-to-trough decline of just over 80%. Other peak to trough declines in names we had puts on include Lucid Motors (-88%), Rivian Motors (-86%), MicroStrategy (-79%) and Tesla Motors (-72%).

To capture this type of a payoff profile, we bought puts outright that were deep out of the money and several months out in time, without structuring them as a put spread which would cap our gains. We were then disciplined to take most of our cost out as these puts went onside early in Q1, allowing us to let them ride as a ‘free option’ and earn many multiples of our premium paid.

We certainly didn’t short them on the highs, nor did we cover them on the lows, but we were able to reap many multiples of the premium we paid as the stocks began to unravel. This helped us protect our core portfolio from the broader market decline.

What occurred in financial markets post-Covid was an exceptional chapter in financial history, and we would caution our investors to note extrapolate those types of returns in the future. While exceptional circumstances will present us the opportunity to earn exceptional returns, a risk-reward setup like we encountered in 2022 just doesn’t come around that often.

Our returns this year were not entirely driven by hedging and active trading gains. Our top performing core holding in 2022 was a new addition, Louis Vuitton Moet Hennessy. We first started buying shares in Q1, and this investment generated over 60 basis points for the fund this year. Shares are up 34% since our initial investment 10 months ago, outperforming the S&P 500 by over 40% over that time frame. We anticipate that when we sit down to write our Q4 commentary in twelve months, we will be crediting our core portfolio for a much larger proportion of our returns.

Looking Ahead

Market participants seem to be overly focused on the idea of an imminent “Fed Pivot”. This is understandable since Powell had to engage in such an about face during the last hiking cycle in late 2018. Investors seem to be focused on a binary outcome of either the Fed tightening or easing. Futures markets are currently pricing in rate cuts before the end of this year – investors are wagering on an outcome where the Fed rapidly shifts from hiking to cutting less than 9 months (assuming March is the last hike). We strongly feel this is misguided, and investors are suffering from recency bias based on the last two tightening cycles.

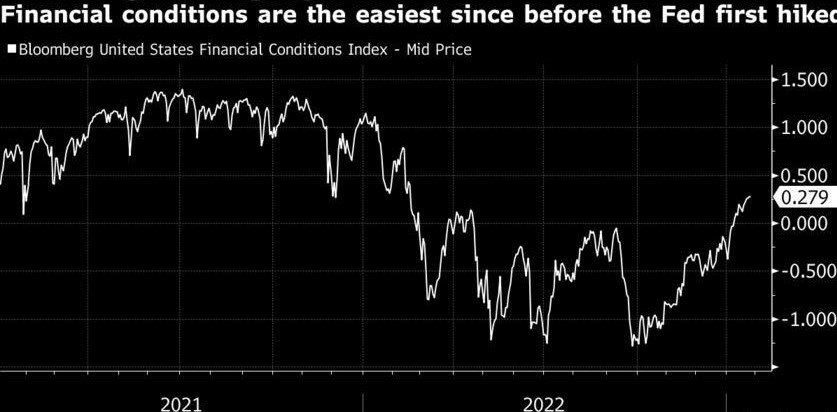

Our view is that a pause does not equal a pivot, and this is an important distinction. Investors need to consider the possibility that after a pause, they may keep rates at that terminal level for much longer than expected. They may pause just to resume hiking again if inflation stays elevated and financial conditions ease further than they want. This would cause a dramatic sell off in stock and bond markets. The chart below shows how loose financial conditions have gotten over the past few months – this does not make the Fed happy.

WHAT TIGHTENING CYCLE?

The following quote from Raphael Bostic, President of the Atlanta Federal Reserve is worth noting:

“We are just going to have to hold our resolve… Three words: a long time. I am not a pivot guy. I think we should pause and hold there, and let the policy work” – Jan 9, 2023

Our view is that the only thing that would get the Fed to cut rates this year would be an unforeseen shock to the markets or economy (which is typical of past global tightening cycles) – in which case the S&P will be trading much cheaper than it is currently.

Where Are We Now?

At 4,030 the S&P 500 is pricing in a very soft landing – in fact almost a Goldilocks scenario. We believe the rally in the market thus far in January is low quality in nature, and appears to be led by short covering in some of the most beat up parts of the market last year. Tax loss selling into year-end is likely exacerbating this behaviour as well. Many of our best shorts from Q1 last year seem to be leading the way in Q1 this year: Lucid Motors +30% YTD, ARKK +20% – not exactly a sign of a high quality rally.

2022 earnings for the S&P should come in around $203, and expectations are for $223 in earning in 2023. This means not only is the market expecting earnings to grow 10%, it is already ascribing an 18.5x multiple to those earnings.

When we’re putting on hedges, we don’t simply focus on how much money we stand to make if we are right, but equally important, how much we stand to lose if we are wrong. At a peak multiple of an inflated earnings figure, we just don’t see the S&P 500 getting away from us on the upside, thus we remain defensive.

Best of all for Lions Bay, given the strong start to the year for equity markets, volatility is back to being attractively priced relative to these risks. The VIX is now back to an 18 handle, down over 12.5% from where it closed the year.

Where We Are Hedging

This time last year, the speculative growth sector made no sense to us, and betting against some of these stocks represented one of the most attractive risk reward set ups we’ve ever seen. As a bear market goes on, it becomes harder and harder to find attractive shorts/hedging candidates. Most of the pain has occurred in the most obvious sectors of the market, and generally speaking pessimism is high. While we may not see the conditions for the type of outsized returns we were able to generate with the popping of the speculative bubble, we still believe we can identify some anomalies in certain areas of the market.

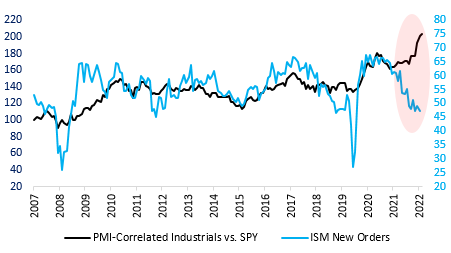

The industrials space, to us, has gotten quite disconnected from fundamentals, and is not reflecting the risk of a prolonged and global economic downturn. We believe investors crowded into this space on optimism of China re-opening, and a desire to participate in businesses that benefit from rising inflation. We believe inflation has peaked, and our experience as Canadians has taught us that re-opening an economy after lockdowns is seldom a linear process.

The chart below highlights the discrepancy between where industrial stocks are trading and the hard data – the Institute of Supply Management (ISM) New Orders index. We have bought puts on a number of large industrial stocks as well as the relevant ETF.

PMI-CORRELATED INDUSTRIALS VS. ISM NEW ORDERS

What are Companies Doing and Saying?

We believe this earnings season is critical to our outlook for the year, and we have seen a lot of commentary, as well as strategic decisions, that reinforce our view that the prevailing view on earnings growth is overly optimistic.

Layoffs are happening in a big way, in particular in the former tech darlings that were such a large part of the market recovery coming out of the pandemic. Many of these businesses over-earned as they benefitted from either a pull forward in demand or demand from one-off events.

See below for how staggering the growth in head count has been at many of these companies. As they rapidly adjust their cost structure to slowing demand, we are witnessing many layoffs in the sector – most of which are high paying jobs.

- Amazon: 229,000 (2016) to 1,540,000 (2022)

- Microsoft: 114,000 (2016) to 220,000 (2022)

- Apple: 100,000 (2016) to 164,000 (2022)

- Meta (Facebook): 13,600 (2016) to 87,300 (2022)

- Alphabet (Google): 60,000 (2016) to 187,000 (2022)

- Salesforce.com: 25,000 (2016) to 80,000 (2022)

Companies telling us on earnings calls that margins are vulnerable. Delta Airlines just reported on their call that airfares were declining despite a recent need to give pilots a huge wage increase (34% over 4 years). Banks are also signalling caution, as JP Morgan reported rising delinquency rates require extra reserves to be set aside.

Some other datapoints from a variety of industries include:

- Lululemon cutting guidance and margin forecast at a recent industry conference

- Tesla cutting prices repeatedly across Europe, US and Asia in order to stimulate falling demand

- KB Homes reporting a drop in home orders

- Goldman Sachs embarking on its largest round of job cuts ever

- Blackrock laying off 3% of its work force citing ‘unprecedented market conditions’

- Fedex scaling back deliveries on faltering e-commerce demand

As Nancy Lazard from Piper Sandler recently highlighted, slowing inflation poses a very real risk to corporate America, as much of the post-Covid profit growth has been nominal, while many of the cost increases to account for tighter labour have been structural (see Delta above). As nominal prices normalize (e.g. air fares, used car prices etc.) and wages remain sticky, margins and therefore earnings will suffer.

We just don’t see a “Goldilocks” type outcome given an environment with declining revenues and rising unemployment.

At some point this year we will see rapidly rising/peaking unemployment claims, signs of bottoming in the housing market, and a more convincing washout of investor sentiment and price multiples. Those are the preconditions we will be watching for to get more aggressively invested on the long side. Unemployment is historically a lagging indicator, thus when it starts rising rapidly it’s usually time to start buying stocks.